Meet Our Consultant Team

If you would like to know more about Construction Finance please call Peter, Simon or David on 03 9882 2500 or email;

First Point Group hosted a successful First Home Buyer Information evening in August. We teamed up with two of our trusted referral partners at Garcia & Jones (Property Buyer & Seller Advocates) and Merton Lawyers to provide a relaxed and informal information session, specifically for potential first home buyers.

The aim of the evening was to help educate the 40 attendees who hope to embark on their first home buying journey in the not too distant future. Topics covered included:

It was fantastic to have the opportunity to provide information to the next generation of home buyers to give them the confidence they need when they are ready to purchase.

If you would like any information about the topics covered above, please Contact Us.

If you would like to know more about Construction Finance please call Peter, Simon or David on 03 9882 2500 or email;

Are you thinking of building a home or completing a significant renovation?

How does a Construction Loan work?

A normal home loan will advance all funds on the settlement day, e.g. when you buy an established home, generally all the loan funds are paid to the vendor.

For a construction loan, the loan funds are progressively drawn down as each stage of construction is completed by the builder. These payments are called Progress Payments and are paid directly to the builder by the lender. With each payment to the builder, your home loan increases.

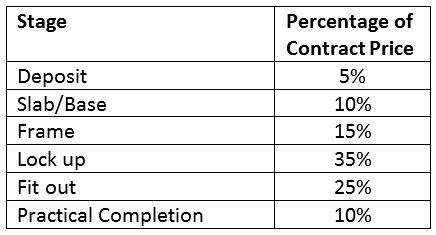

A typical builder’s contract will include Progress Stages which might look as follows:

Payments during Construction

Loan repayments during the construction period are Interest Only, which means interest is only charged on the funds that have been drawn down at any point in time. In other words, your home loan repayments would typically start out very small, and gradually increase throughout the building process.

Once the final progress payment is made and construction is completed, the Lender will typically inspect the property to ensure it is completed as per the contract and plans that were originally presented. The lender would then pay the final amount to the builder, and your loan repayments will usually convert to Principal & Interest at this point.

What about Contract Variations?

If you and the builder agree to make a minor variation to the original contract, the lender will simply assess whether they have enough funds remaining in the loan to complete all remaining progress claims, as per the original contract. Any additional variation costs will come out of your own funds, and any cost reduction variations, can be paid into your account after the completion of the project.

What Documents Are Required?

Below is a list of documents required by a lender as part of a construction loan application:

Once the loan is approved, and before the first progress payments are made to the builder, the following documents would be required:

With your signed Progress Payment Form and the other documents in hand, the lender will release each stage payment directly to the builder’s account.

Most lenders will send an independent Valuer to inspect the property at the first and last stages of construction.

First Point Group was recently able to work with the Federal Government Export Finance Insurance Corporation (EFIC) and a major Bank to deliver a working capital/trade finance solution for a rapidly growing exporter.

At the same time, we arranged a refinance of the client’s personal mortgage from a smaller regional bank to the Major bank where the trade finance was organised, resulting in a better deal overall.

This was a case of a client outgrowing a smaller Lender that suited their requirements in the early days of business, but now required a smarter and more sophisticated and higher level of funding to free up cash flow and allow further growth into overseas markets.

It was determined a major bank was the best fit for the client when considering the market they operated in.

First Point Group recently organised funding for a client to purchase a Student Apartment complex (multiple) in Melbourne. The student apartment market is changing, consolidating and complex.

We needed to navigate through complex Lender policies to ensure we ended up with the right Lender fit for the client in relation to the loan structure, pricing and effective Loan to Value Ratio (LVR) that met the client’s needs.

This was a complex transaction and the clients were very satisfied with the outcome.

1. Reduce credit card limits

If you have credit cards, each card will have a credit limit, and those credit limits are considered when your home loan application is assessed – that means your credit limits will reduce your borrowing capacity, whether you use the full credit limit or not!

If you have $20,000 in credit card limits, but you can live with $5,000, you should reduce your credit limits before you apply for a home loan.

2. Self Employed?

Tax time is approaching. If you are a self-employed person running a business with partners, and you are not “in control” (i.e. you own less than 50% of the shares), banks/lenders will be reluctant to take your business profits into account unless the profit is making its way out of the business to you, or an entity that you own 100%.

If you do not have “control” over profit distribution decisions and your business/partnership has retained its profit, most lenders would be unlikely to take that income into account.

If the profit makes its way down to you or your family trust, you may subsequently pay income tax, but you will also improve your borrowing capacity.

3. Consolidate Existing Debts

Unsecured debts (credit cards, personal loans etc) often have a higher rate of interest than any home loan products, so consolidating any debts that have short repayment terms with expensive monthly repayments is a good idea. These debts significantly impact your home loan borrowing capacity. If you’re refinancing your current home loan, you can roll your personal loan or other debts into your existing mortgage.

4. Demonstrate Your Savings Ability

When a bank/lender conducts their ‘serviceability’ review of your income vs. your expenses, your loan would only be approved if there is surplus income each week/month. The lender will then look to your current savings accounts to see that you have actually been saving this ‘surplus’, not spending it! It is a good idea to have a proven track record of savings -eg. 3 to 6 months.

5. Check Your Credit History

Lenders look at your credit score or credit rating to work out if they should lend you money or give you credit. Your credit score is a number based on an analysis of your personal credit file, at a particular point in time, that helps a lender determine your credit worthiness. The modern credit reporting system will show a prospective lender:

More information about your own credit file can be found on these websites:

https://www.getcreditscore.com.au

https://www.moneysmart.gov.au/borrowing-and-credit/borrowing-basics/credit-scores

Our website has many different finance calculators available to help you

Our website has many different finance calculators available to help you

Many small and medium businesses have struggled in the current environment to obtain working capital finance quickly and efficiently.

Many Lenders are happy to assist, but only when property is offered to secure the loan. Additionally, the approval and settlement process can take a considerable length of time.

First Point Group have connected with a number of Lenders within the business lending market who are able to provide short term and unsecured finance with speed and relative ease.

Here are some points to consider:

Eligibility requirements:

Please contact Peter, David or Simon if your business has a working capital requirement.

Follow these tips for a welcoming garden that’s filled with colour and fragrance.

Make note of tree limbs that should be removed, especially those that overhang structures. Cut down last year’s perennial foliage and throw it into the compost pile. Rake mulch from beds planted with bulbs before foliage appears, and refresh mulch in other planting areas after soil warms. Check fences, steps, and pathways for signs of damage.

Clean up your garden tools so everything is ready when things start growing. Choose new plants for the garden for spring planting.

Send the mower and leaf blower for servicing, or if you have the right tools, sharpen the mower blades yourself. Refill your mower with oil, install fresh spark plugs, and lubricate moving parts if necessary. Clear the lawn of winter debris, and look for areas that need reseeding before mowing.

Remove dead, damaged, and diseased branches from woody plants. Thin and trim summer-blooming shrubs such as butterfly bush, hydrangea, and most roses. Prune spring-blooming shrubs and trees after flowering.

Check soil pH with a home soil test kit, taking several samples from different planting areas for an accurate reading. Enrich soil as necessary: Add dolomitic lime to raise the pH or elemental sulfur to lower the pH.

Clear the planting area as soon as soil can be worked, removing weeds and debris. Spread a 50mm layer of compost or manure over soil with a spading fork.

Plant bare-root trees, shrubs, and perennials by early spring. Choose a cool, cloudy day if possible. Sow seeds of cool-season flowers like sweet peas, poppies, and vegetables such as lettuce, parsley, and spinach.

Apply balanced fertiliser recommended by soil test results around trees and shrubs when new growth appears. Begin fertilising perennials when active growth resumes.

Start a compost pile, or use a compost bin, if you don’t have one already. Begin by collecting plant debris and leaves raked up from the garden. Add equal amounts “brown” (carbon-rich) materials like dried leaves and straw and “green” (nitrogen-rich) materials like grass clippings and weeds in even layers with water and a compost bioactivator.

Disinfect the feeders by scrubbing with weak bleach solution (250ml bleach : 1 litre warm water). Rinse and dry the feeders thoroughly before refilling them. Scrub birdbaths with bleach solution, then rinse them thoroughly and refill, changing water weekly.

Finance Insights – Summer 2019

Finance Insights – Summer 2019